When confirmation isn't departure

Two prediction markets, one Fed Chair transition, and an 86-point round trip in 36 hours

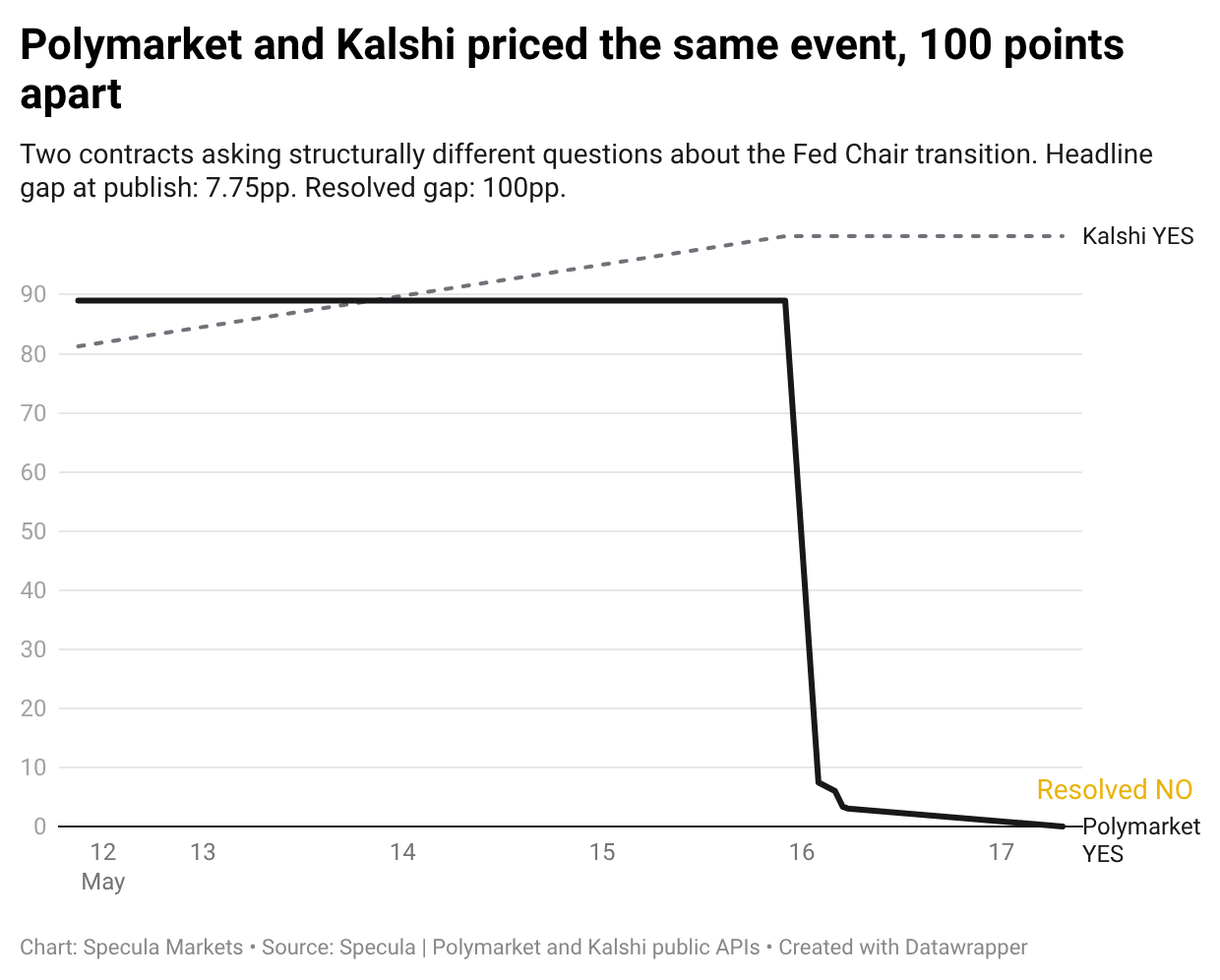

On Friday afternoon, Polymarket priced “Will Jerome Powell depart as Fed Chair by 16 May 2026?” at 89% YES. By 02:00 BST Saturday morning, the same contract traded at 7.45% YES. By the resolution deadline 24 hours later, it had settled at around 3% YES. The market resolved NO at 07:21 BST Sunday.

In the same window, Kalshi’s “Will the US confirm a Federal Reserve Chair pick by 15 May 2026?” contract resolved YES. Kevin Warsh was sworn in on Friday. Jerome Powell remained on the Board of Governors and continued in the Chair role for the brief transition handover.

Same underlying event. One market YES, the other NO. The headline gap between the two venues, which sat at 7.75 percentage points when we wrote about it on 12 May, peaked above 80 points and resolved at the maximum possible value of 100 points.

This is what the resolution-criteria gap looks like in full.

The two contracts

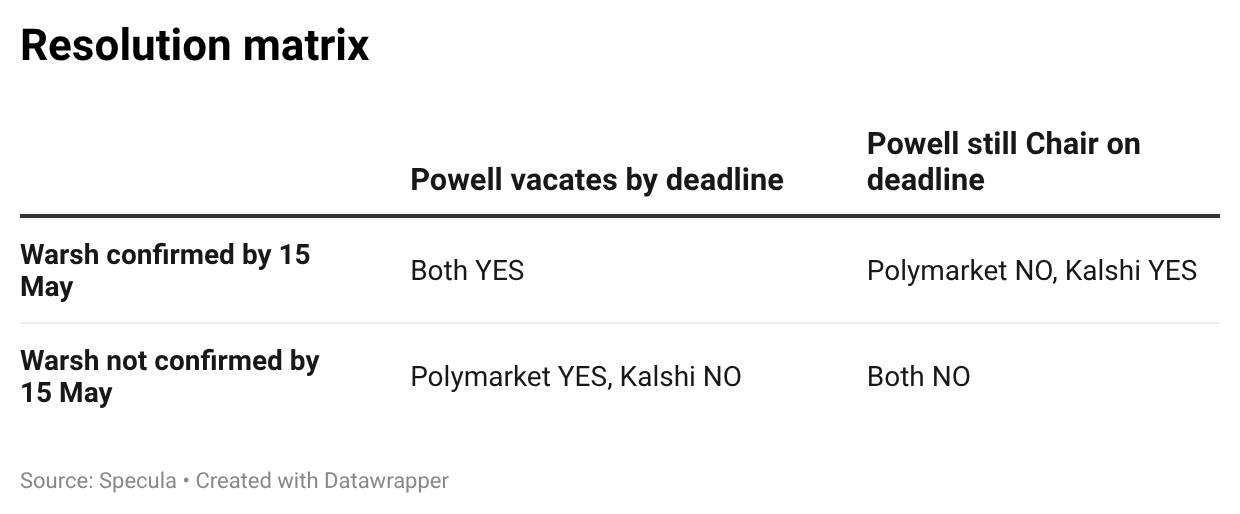

Polymarket listed “Will Jerome Powell depart as Fed Chair by 16 May 2026?” with a resolution criterion that required Powell to actually vacate the role. The contract description was explicit: “Announcements of resignations or firings will not alone qualify. The scheduled end of Powell’s term as Chair will not alone qualify. If Powell continues to serve as Chair on a temporary basis (e.g. until the confirmation of his successor), he will not be considered to have vacated his role as Chair.”

Kalshi listed sub-markets under “When will Kevin Warsh be confirmed as Fed Chair?” with the date ladder Apr 1, May 1, May 15, Jun 1, Jul 1, Aug 1. Resolution required only Senate confirmation by the listed date, regardless of whether Powell had vacated the Chair role.

Two contracts, one news event, structurally different questions. The matrix:

Until late Friday, market consensus sat in the top-left cell. Senate confirms Warsh, Powell hands off the Chair, both markets resolve YES. The 89% Polymarket price reflected that consensus. The 7.75 percentage point gap to Kalshi at our 12 May piece reflected mild uncertainty about timing of step-down, not disagreement about direction.

What actually happened was the top-right cell.

The 82-point repricing

Sometime in the four hours between 22:00 BST Friday and 02:00 BST Saturday, the Polymarket contract collapsed by 82 percentage points. The 22:00 snapshot caught it at 89% YES on $51 of 24-hour trading volume. The 02:00 snapshot caught it at 7.45% YES on $13,950 of volume.

Nothing about the underlying event changed in those four hours. Kevin Warsh was still the confirmed nominee, sworn in earlier on Friday. Jerome Powell was still on the Board. The Senate had voted Wednesday. The Reuters Breakingviews piece reading Warsh’s likely tenure as Chair was already public. What changed was how participants read the resolution criterion.

Two things became clear in those hours.

First, Warsh’s swearing-in on Friday was as Chair-designate. He has begun work and has the role, but the formal handover from Powell was structured to occur at a defined point that postdated the 11:59 PM ET 16 May deadline.

Second, Powell’s continued service through the brief transition window, while Warsh prepares to assume the Chair role, falls squarely inside the contract clause that “if Powell continues to serve as Chair on a temporary basis (e.g. until the confirmation of his successor), he will not be considered to have vacated his role as Chair.”

The Senate had confirmed. The Chair role had not yet been vacated. Kalshi’s question resolved YES. Polymarket’s question resolved NO.

The price found the right level in the four hours when serious volume showed up to read the contract. The remaining 24 hours of price discovery from 02:00 Saturday to the 04:59 BST Sunday resolution deadline saw a gentle drift from 7.45% YES down through 3.05% YES, with the contract settling NO via Polymarket’s automated UMA oracle at 07:21 BST Sunday.

Why this matters for cross-venue analysis

The 12 May piece argued that Polymarket and Kalshi list the same world but ask different questions. The 7.75 percentage point gap was the first illustration. The 100-point resolved gap is the second, much larger one.

Three points worth noting.

One: a single number understates the divergence. If you watch only the headline prices, the gap between Polymarket and Kalshi looks like price discovery. Both venues converge on a similar number for a similar question, with some residual disagreement. When the gap widens dramatically near resolution, the natural reading is that one venue is finding the right price faster than the other.

That reading misses what is actually happening. The wider the gap gets, the more it suggests the two markets are not asking the same question at all. The right interpretation isn’t “one market is wrong.” It’s “these markets resolve on different criteria.”

Two: resolution criteria are the moat for analytical work. Anyone can pull the headline price from Polymarket or Kalshi. The question is whether the headline price answers the question you care about. For the Fed Chair transition, an asset allocator watching “what happens to monetary policy now” would not have been well served by either market in isolation. The Polymarket contract was about a procedural detail of when Powell formally stepped back. The Kalshi contract was about Senate timing. The thing an allocator actually wanted to track, which is when Warsh begins setting policy and what he does first, was not directly listed on either venue.

Three: the news flow during a structural reveal is often more informative than the price. The 22:00 BST Friday market sat at 89% YES on essentially no trading volume. Participants weren’t disagreeing. They were not paying attention to the resolution clause. By the time meaningful volume arrived four hours later, the price had collapsed. The information content was not in the slow drift; it was in the late repricing. For any cross-venue work that wants to track what markets actually think versus what markets have priced from inattention, the velocity of repricing matters as much as the level.

The Warsh question

The cleaner framing of this transition is one neither market is directly listing. What does Warsh do in his first 90 days, and how do prediction markets price the path of monetary policy under a chair who has publicly criticised the Fed’s communications strategy?

Reuters Breakingviews this weekend made the case that Warsh’s stated preference for a quieter Fed, more humble about predicting the future, fits a moment when the Fed’s own forecasts have been overrun by an oil shock that nobody in the FOMC predicted. Projections for rate cuts in 2026 have dwindled from two to zero. Long-term Treasury yields have risen above 5%. If Warsh follows through on retiring forward guidance and the dot-plot, market-implied expectations from prediction markets and rate-futures pricing will carry more weight as a read on crowd-implied expectations, precisely because the official Fed channel will be deliberately quieter.

That makes cross-venue prediction-market data more useful, not less, in the next 12 months. The work of reading the contract before reading the price applies just as much to “Will the Fed cut at September FOMC?” as it does to “Will Powell depart as Chair by May 16?” The lesson is the same one.

The methodological note

Specula maintains a canonical events layer that maps prediction-market contracts to underlying events and notes where the resolution criteria differ. For the Fed Chair transition, the canonical event flagged the resolution-criteria gap on 12 May, before the late-Friday repricing made it visible in price terms. The cross-venue divergences we surface are not noise to be smoothed over. They are often the most informative thing in the data, and they are best read against the resolution criteria rather than against each other.

For this transition, the headline gap was 7.75 percentage points at publish, peaked above 80 points in the 36 hours before resolution, and finally resolved at the maximum 100 points. The lesson, in any future cross-venue analysis: read the contract terms before reading the prices.

Specula provides data and derived metrics on prediction markets. Not investment advice. Methodology and underlying data available at terminal.specula.markets.